The basic strategy for any DIY retirement planner based in the United States is to accumulate as much pension as possible in the Roth IRA.

Roth IRA’s contributions and conversions have increased tax exemption, with withdrawals exemption and not subject to the required minimum distribution (RMD).

I didn’t have a Roth IRA for the first 15 years of my investment career.

Roth Iras, acquired in 1998, spent some time adopting by discounted online brokers and small investors.

From 1995 to 2010, I invested primarily through employer-sponsored 401(k) programs, traditional IRAs and taxable accounts (including brokerage accounts and drip).

I will first maximize my retirement account and then invest any remaining cash into my taxable account.

My Fidelity Taxable Investment Fund (formerly before TD Ameritrade) has grown significantly since 1995, generating more than $1,000 in dividend income per month.

Due to irregular revenues in my business, I use some of these funds to supplement my spending needs.

But taxable accounts are generating dividend income surpluses. Instead of reinvesting the dividend back into the investment in the same account, I transferred the cash to my Roth IRA as a contribution.

This strategy reduces the future tax burden (contraction) of taxable brokerage accounts, makes Roth IRA obese, and frees up my living expense income.

Can Ross donations come from taxable brokerage accounts?

Yes.

You must have earned money to be eligible to donate, but donations can come from multiple sources, including checking, savings and taxable brokerage accounts.

Most people contribute Roth Iras from their income.

Roth IRA contributions must be cash donations, not physical transfers (stocks).

Therefore, brokerage account holders can sell investments or accumulate dividends before donating to Roth IRA.

Selling an investment can induce capital gains and related taxes, so if you consider selling an investment in a taxable account to make a Roth donation, you need to do a thoughtful tax.

My recent Rose contributions are mostly from dividends, but over the next decade, I have also sold some investments, which is part of my simplified strategy, reducing the number of individual stock holdings to support ETFs and mutual funds.

video

Watch the video:

automation

If possible, donating at the beginning of the year is the best option. If you have funds available, the total investment in investment investment is better than the U.S. dollar cost.

If not, another way to contribute regularly without emotional risk is to automate Roth’s contribution.

If your taxable account initiates enough dividend income, you can divide the donation limit by 12 and automatically transfer equal amounts on the same day of each month.

Then, set up automatic purchases in a few days.

That’s how I initially set it up, but due to the upcoming travel expenses, I decided to hope to be more flexible in the coming year.

Currently, I set up a monthly reminder and make manual contributions and investments. After the big spending is liquidated, I may return to automation.

Roth IRA 2025 donation restrictions

I’m 50 years old this year, so I can contribute $1,000.

| Roth IRA 2025 Contribution Limits | |

|---|---|

| Basic contribution limits | $7,000 |

| Chasing Contribution (over 50 years old) | Extra $1,000 (total: $8,000) |

Roth IRA 2025 Revenue Limits

My work is now more fulfilling. But since I left my full-time consulting career, my income has dropped significantly. So we don’t always have enough revenue to make consistent Roth donations.

Lower income makes it eligible for Roth IRA contributions.

If I meet the following limits, I can use the SEP IRA contribution to reduce my modified adjusted gross income (MAGI) and maintain eligibility – a nice benefit for business owners.

This is the 2025 Roth IRA income limit list. These values continue to rise with inflation (see the figure below).

At least 85%-90% of single-tax filers will receive Roth IRA donations in 2025, while more than 90% of co-applicants with married applications will be eligible.

If possible, prioritize the early stages of Ross’ career.

| Application Status | Modified AGI (MAGI*) | Contribution limit |

|---|---|---|

| Single or ancestor | Less than $150,000 | Up to $7,000 ($8,000 if age 50 or older) |

| Single or ancestor | $150,000 – $165,000 | Reduce contribution |

| Single or ancestor | Over $165,000 | Not eligible |

| Married co-submit | Less than $236,000 | Up to $7,000 ($8,000 if age 50 or older) |

| Married co-submit | $236,000 – $246,000 | Reduce contribution |

| Married co-submit | Over $246,000 | Not eligible |

| Married submissions (Living with your spouse every year) |

$0 – $10,000 | Reduce contribution |

| Married submissions | Over $10,000 | Not eligible |

* MAGI: Starting with the adjusted gross income (AGI) of Form 1040, plus IRA contribution deductions, student loan interest deductions, tuition and expense deductions, passive loss or income amounts, loss of leased property, half of self-employment tax, half of adoption expenses, adoption expenses, income exclusion, income savings bonds obtained from public trade groups, partnership losses, partner losses obtained from public trade groups.

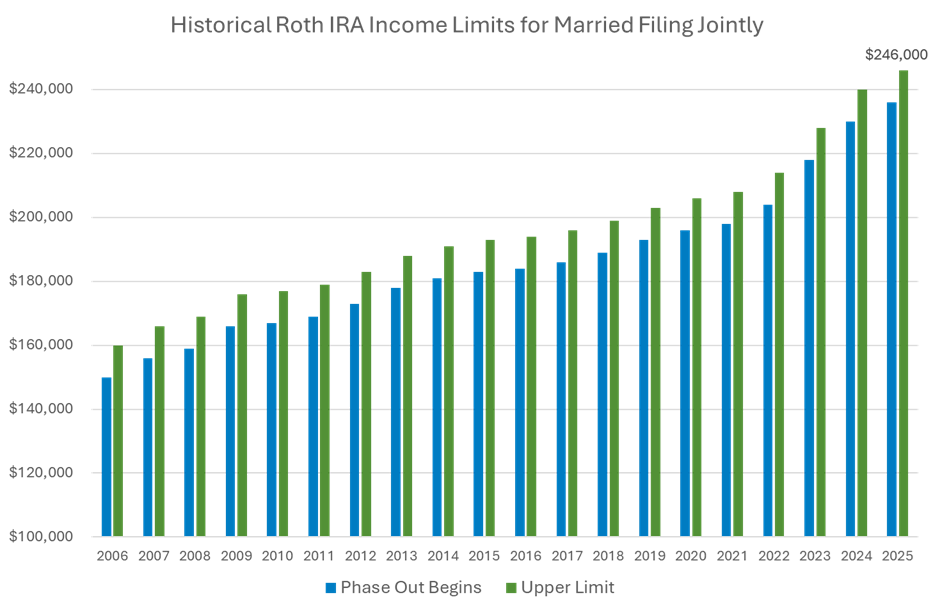

History of Joint Married Applications Roth IRA Income Limit

Here is a Roth IRA income limit chart since 2006, co-filing for married taxpayers.

Simplified DIY investors

In many of my years of work, I chose to contribute to a traditional IRA to reduce taxable income for taxable years rather than Roth IRA.

I don’t regret it, but when I got the chance, I could have contributed more aggressively to Ross.

This became my plan last year when I could contribute from my taxable brokerage account.

Now that we are qualifying for Rose again, donations have meaningfully helped narrow taxable accounts and reinvest the proceeds in more efficient accounts.

As long as it makes sense, I will convert a large amount from taxable accounts and pre-tax IRA (convert) to tax-free growth tools.

Together, Mrs. RBD and I can donate $15,000 in 2025. If possible, we will make the most of the revenue from both accounts, depending on spending needs and my business income.

This manipulation fits with my 10-year simplification strategy to simplify my portfolio and is beneficial for long-term tax plans.

Roth IRA’s money is likely the bank that I’ll touch on in retirement.

Featured images are performed through photos of deposits used by license.

Craig Stephens

Craig is a former IT professional who left his 19-year career to become a full-time financial writer. He has been a DIY investor since 1995, and he began retirement in 2013 as a creative outlet for sharing his portfolio. Craig studied finance at Michigan State University and lived in Northern Virginia with his wife and three children. Read more.

Favorite tools and investment services (sponsored):

Travel Reward Card – My spending and travel rewards credit card.

Authorization – Free Net Worth & Portfolio Tracking + Retirement Plan. Users since 2015.

Boldin – Insufficient spreadsheets. Build financial confidence. (Review)

Determine dividends – Free download of research dividend stocks (comments):