I’ve been attracted to me since I was a child Not conducive to interest – Have enough income to generate cash and investment assets for retirement dividends and interest No principal spent.

This is attractive because it will provide the ultimate sense of financial security.

When investors are able to generate enough income to cover living expenses, they have already achieved Cross-border points – Concepts introduced in the 1992 book Your money or your life.

Most people, myself, may never reach the intersection of investment income because it is unnecessary.

You can use the Safe Withdrawal Guide (withdrawal of 4%-5% of investment assets – “4% Rule of Thumb”) to merge dividend income and generate income from investment sales to retire as soon as possible.

Dividend income and distribution of stocks, ETFs and mutual funds will play a big role in my retirement, but most of my wealth is in low-yield market growth assets (such as FSKAX) that I can sell to generate income when needed.

Market Growing Assets (designed to get total return) – Grow your portfolio and protect it from inflation to prevent the currency from running out after retirement.

It seems very attractive Retirement dividend Alone, A combination method More realistically, it allows you to retire soon, spend more money, enjoy yourself and avoid becoming miserable.

Retirement example on dividends (income portfolio)

For example, suppose your annual expenditure is $100,000. To make so much money every year, you need:

- $5,000,000 investment with a yield of 2.0%

- Invest $4,000,000 with a 2.5% yield

- $3,333,333 investment with a yield of 3.0%

- $2,500,000 investment with a 4.0% yield

- $2,000,000 investment with a 5.0% yield

We will assume that the income is generated and consolidated in a tax preferential account.

When I wrote this, the S&P 500 produced about 1.2%. Therefore, the purchase market The only one Living from dividends will require more than $8 million.

But if you invested $8 million and you only spent $100,000 a year to retire – you are a cheaper person and should enjoy yourself more!

As investors focus more on higher-yield investments, the long-term growth prospects will decline. Think of NVIDIA and ATT as extreme example.

A diversified dividend stock portfolio can outperform the S&P 500, but requires a lot of work and luck. In the long run, most stock pickers won’t outperform the market.

While higher-yield portfolios will abandon more income, focusing on income rather than total returns will reduce total returns and wealth over time.

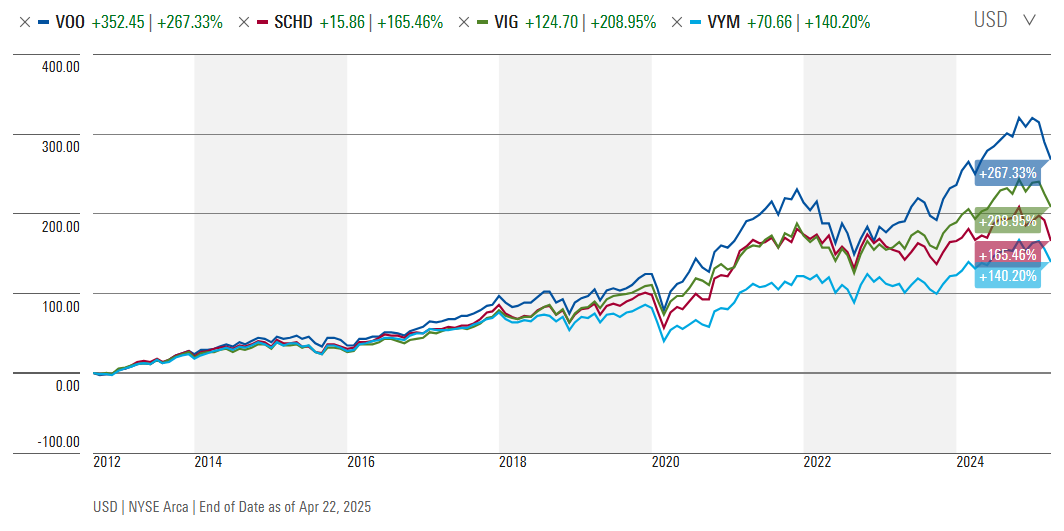

For example, since 2012, the S&P 500 ETF (VOO) has easily outpaced these popular dividend-centric ETFs.

That said, investments that generate income can help in market recession because if you rely on investment, it is psychologically difficult to sell investments when the market falls.

Mitigate psychological risks by holding more liquid cash and bonds.

With a balanced withdrawal strategy, income-generating assets and investment sales are consistent with a balanced portfolio and investor mentality.

Example of investment sales (capital income) (S&P 500 portfolio)

Let’s take the same example as an example and assume that investors reinvest all dividends in the security of paying them. Investors use investment sales only to generate revenue for their annual spending needs of $100,000.

Since the 1990s, the safe evacuation rate of rule of thumb is 4%. But Bill Bengen, a financial adviser who runs the original mathematics behind the number, now says most investors can use 5% based on the latest research and portfolio management.

So I’ll use 3% (conservative) to 6% (more aggressive but suitable for many) and tax benefits to keep the scope simple.

To safely withdraw $100,000 per year, we need investors:

- $3,333,333 investment, with a 3% withdrawal each year.

- $2,500,000 investment, withdraw 4% per year

- $2,000,000 investment, with 5% withdrawn annually

- $1,666,667 investment, with 6% withdrawn annually

Note that the math is the same as the example above.

The difference is that growing portfolios (e.g. buying only the S&P 500) aims to have higher overall returns, while the revenue portfolio aims to increase yields.

Check the image above again to see which wins.

With the help of the method of returning the market, using only asset sales, you will have more wealth and money as the market may outperform the market.

Is money better than small money?

I said that tongue because a somewhat famous fire master told me for many years.

However, absolutely operation is unrealistic, especially in personal finance and retirement plans.

Real estate: a combination of the two

A combination of income that does not require any major reductions may blur investors with warmth of financial security.

The reality is that most people have growth and income (stocks and bonds).

Moreover, it is absolutely OK to add higher investments (including dividend stocks, ETFs, bond funds, CDs, etc.) in good or bad markets.

These investments reduce volatility and risk and provide age-appropriate stability and stable income.

In 2023 and 2024, this may not matter.

But now that the market has fallen, people living from secure withdrawals may feel uncomfortable with the investment in sales expenses, although the rules of thumb will do in any market environment over the past 100 years.

Pensions, Social Security, annuities, part-time income and other reliable sources of income usually provide an income benchmark. Safe withdrawals usually play a role in supplementing income.

Additionally, if you do not reinvest, dividends and distributions of stocks and bonds funds will naturally fill in your cash account. Selling assets may not always be necessary.

I would rather hold a growing asset that is primarily about supplementary bonds and dividend-centric assets that will aggregate distributions into healthy cash and short-term accounts to cover the fees for several months (providing a buffer).

Then, click on the cash account when needed.

I’m not at this stage of financial planning and life.

But I use some dividend income to supplement our household expenses because my business income fluctuates monthly, so I can imagine what it was like when I retire.

Another advantage of dividend income is that it eliminates a layer of emotional behavior. As revenue automatically enters, the demand for selling assets decreases.

When investing in sales revenue, it is best to set up automation and sales regularly to eliminate potential sentiments attached to market transfers.

in conclusion

There is still an attractive appeal without any dividends at all – it’s a symbol of financial independence, your money works, so you never have to need it anymore.

But sticking to that dream too closely can lead to retirement delays or becoming an abuser.

The insight here is not about dividends or capital gains, income or growth, or even hitting a magical number.

It’s about financial security and developing a financial strategy that aligns with your retirement needs and inevitable uncertainties.

Retirement finance is not a mathematical rigidity – it is flexible. The goal is to have a good time at night.

Some may choose to prioritize rich financial security – spend less money and plan to leave the legacy – while others will spend on less conservative levels to “died from zero.”

Ultimately, many retirees of wealthy retirees are still unnecessarily afraid of running out of money and not spending too much on retirement.

Their children will thank them.

Don’t guess. Use DIY planning tools, e.g. Boldin (Comment) or projection (Review).

Featured images are performed through photos of deposits used by license.

Craig Stephens

Craig is a former IT professional who left his 19-year career to become a full-time financial writer. He has been a DIY investor since 1995, and he began retirement in 2013 as a creative outlet for sharing his portfolio. Craig studied finance at Michigan State University and lived in Northern Virginia with his wife and three children. Read more.

Favorite tools and investment services (sponsored):

Authorization – Free Net Worth & Portfolio Tracking + Retirement Plan. Users since 2015.

Boldin – Insufficient spreadsheets. Build financial confidence. (Review)

Determine dividends – Free download of research dividend stocks (comments):

Fundraising – Simple real estate and venture investments are only $10. (Review)

– Retirement Research Center")