If health care in the United States wasn’t so expensive, more people would retire earlier and live better, happier lives. We are one of the few countries in the world that ties affordable health care to employment, which makes achieving financial independence even more difficult.

Given the high cost of insurance, before you decide to retire early, try negotiating a severance package and use your last year of work to get into the best shape of your life. Think of it as an investment in future health dividends. The stronger and healthier you are, the less you need to rely on expensive medical care. Additionally, the longer you can extend your free money.

Considering the medical expenses, I decided to voluntarily retire early

When I voluntarily retired in 2012, one of my biggest concerns was figuring out how to pay my medical bills. For 13 years, my employer has subsidized part of my premiums through a group plan. Instead of paying $850 a month for insurance, I only paid about $375 at the end.

So when I got off work, after the 6 months of 100% medical subsidy as part of my severance package ran out, I was faced with an $850 monthly bill as a healthy 34 year old who had barely used the system. It felt like it was too much and I needed a plan.

At the time, I asked my wife of 31 years not to let YOLO give up my career. Instead, I encouraged her to embrace equality and continue working for three years to ensure that my seemingly reckless move did not put our family in financial jeopardy. Thankfully, she agreed.

During that time, she maintained an employer-sponsored health care plan, which also covered me. Regardless, many of her colleagues have home insurance, so it’s completely normal to join her plan.

Our medical care is expensive

In 2015, when she was 34, we finally initiated a layoff plan for her, and she would receive a severance package as a high-performing employee. We knew we were going to lose health care subsidies and would have to pay approx. $1,680 per monthbut it is a conscious choice we make in exchange for freedom. It feels wrong to manipulate our income just to get government health care subsidies when we can afford to pay full price.

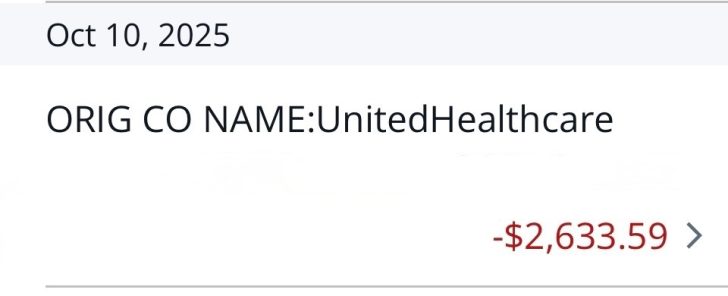

Today, we are a family of four and we pay $2,633.59 per month There are no unsubsidized premiums for the Silver plan, or even for the Gold or Platinum plans. Even though the government calls it the Affordable Care Act, $2,633.59 still sounds unaffordable to me. But the way the system works is that those who earn more than 400 percent of the federal poverty level subsidize those who don’t.

Essentially, we have a high-deductible health insurance plan. I hope my new investment in value stock UnitedHealthcare will help us pay our premiums going forward.

Many millionaires get subsidies for early retirement

The reality is that many early retirees take advantage of Medicare subsidies—even if they are millionaires or multi-millionaires. Some people even brag about it online. This always makes me uncomfortable because I suspect the government’s intention is to subsidize the top 10% of wealth holders. Or maybe it is.

For example, let’s say you have a $2 million investment portfolio that generates $80,000 in annual income. As a Dually Unemployed Parent (DUP) with two children, your household income is approximately 250% of the Federal Poverty Level (FPL), which qualifies you for Medicaid subsidies. Remember, the subsidy is always up to 400% of FPL.

This means that a household with a $5 million growth stock-heavy portfolio earning just a 1.3% dividend yield (approximately $65,000 per year) would have about 210% of the FPL to qualify for 50%+ discount About medical premiums. It’s incredible!

Congressional debate on expanding health care subsidies

Congress is currently debating whether Extension of enhanced medical subsidies Households with incomes above 400% of the federal poverty level. Democrats want to make the temporary expansion permanent, while Republicans prefer to restore the original rules.

The Democratic-authored American Rescue Plan Act of 2021 temporarily increases the value of the premium tax credit and expands eligibility to more than 400% of FPL. These “enhanced” subsidies limit household premium costs to 8.5% of income.

Then, in 2022, the Inflation Reduction Act under Democrats extended these enhanced subsidies through 2025. Now, under the Trump administration, those subsidies are set to expire at the end of 2025.

According to the Congressional Budget Office, extending these enhanced subsidies would cost about $350 billion over 10 years, or $35 billion per year. Considering the size of the existing budget deficit, this is not a large number.

Costs return to original track

Without the deferral, KFF said monthly premiums for a 60-year-old couple earning an average of $85,000 a year (just over 400% of the FPL) would increase by $1,900, or nearly $23,000 per year by 2026. If true, that would be a huge expense under the Affordable Care Act. However, this also means that the 60-year-old couple has received at least $91,200 in health care subsidies since the passage of the American Rescue Plan Act of 2021.

If $91,200 in health care subsidies is saved or invested since 2021 (as all renters say they do to justify not buying a primary residence), they have enough money to pay for higher health care premiums over the next four years. At least, that’s what personal finance enthusiasts think.

Efforts to secure subsidies for early retirement millionaires feel uncomfortable

But don’t you feel a little uncomfortable advocating for more medical subsidies for millionaires? If you earn $85,000 a year as a retired couple, that means your pension or investments Valued at $2,125,000 4% safe withdrawal rate! Most people would say you’ll be fine, especially if you’re debt-free. If you’re an early retiree with that kind of net worth, accepting a subsidy may seem downright strange.

CNBC recently reported on an “early retirement” couple, Bill (61) and Shelly (59), whose pension income will reach $127,000 per year by 2026, above the 400% FPL threshold. Their premiums would rise from $442 to $1,700 per month, which sounds more realistic than KFF’s estimate above. Although it was painful, they also enjoyed it $70,000 enhanced premium tax credit From 2021.

However, a $127,000 pension is worth approximately $3.2 million The annuity is worth a 4% return. Should the ACA really be subsidizing retirees with millions of dollars in pensions and investment portfolios? Resources should be focused on those No A six-figure pension or substantial savings. You know, about 85% of Americans don’t have a lifetime pension.

No one in America should suffer a health crisis simply because they can’t afford medical care. Healthcare is a fundamental right. Therefore, it is more logical to shift healthcare subsidies to the lower middle and poor classes.

Capitalize the value of your pension and investment income

Now I’m starting to wonder – would the average American, financial journalist or politician do this? Don’t know how to capitalize the value of an income stream to determine its true value? We do this all the time in finance and in Financial Samurai. Simply take a reasonable return or withdrawal rate (eg 4% or 5%) and divide your pension or investment income by that number.

let us find out capitalized value of pension Various Federal Poverty Level (FPL) income limits based on a family of four:

- $31,200 (100% of FPL): Pension value $624,000 – $780,000. You may be eligible for 100% subsidy and pay 0% Your earnings are used to pay health insurance premiums.

- $43,056 (138% of FPL): $861,120 – $1,076,400 Superannuation value. you may pay 0–2% of income Premiums after subsidies – approximately $0 to $50/month Silver plans in many states.

- $46,800 (150% of FPL): Pension value $936,000 – $1,170,000. you may pay 1-2% of incomeor about $0 to $50/month For the Silver plan.

- $62,400 (200% of FPL): Pension value $1,248,000 – $1,560,000. Estimated payment 2–2.5% of incomeroughly $50 to $80/month.

- $78,000 (250% of FPL): Pension value $1,560,000 – $1,950,000. you may pay About 4% of incomeor $180–$220/month.

- $93,600 (300% of FPL): Pension value $1,872,000 – $2,340,000. you may pay Approximately 6% of revenueor $300–$350/month For the Silver plan.

- $124,800 (400% of FPL): Pension value $2,496,000 – $3,120,000. you may pay Up to 8.5% of incomeor roughly $450–$550/month For the Silver plan.

If your lifetime pension or passive investment income generates $31,200 or more per year (100% of FPL), you’re doing pretty well compared to the average worker or retiree. Therefore, paying little to nothing to the health care system seems unfeasible.

Adapting to a system that embraces the rich

That said, we should view this debate as a reflection of the times and adjust accordingly. as we practice Identity Diversity Depending on who is in power, we can rely on our wealth when the government decides to subsidize the rich.

If the government wanted to subsidize health care to six-figure pensioners and millionaires, the rational economist in me would say: take the free money. After all, most politicians are over 40 and already wealthy, so it’s only natural that they design policies that benefit their country’s population.

However, the political winds are always changing. When they do, policymakers refocus their efforts on helping the real middle class and the poor, and the rich will once again pay full freight.

Will continue to pay full shipping costs to help U.S.

At our current level of passive income, we will never qualify for Medicare subsidies. Our household expenses are also too high to artificially lower our income. This is probably what happened. For the greater good of society!

In the meantime, I will continue to do my best to stay in shape so that I can subsidize and make room for those who can’t or won’t. Just as it is a privilege to pay taxes to support those who pay less or no taxes, it is also a privilege to have enough health to help offset the costs of those who pay no taxes.

Readers, do you think the government should work to subsidize health care for the wealthy? Or is it irresponsible to expand these enhanced tax credits, given our huge budget deficit? Where do we draw the line when it comes to subsidizing health care?

Tips to protect your life

In addition to exercising regularly and eating healthy to live longer, you should also protect your life with affordable term life insurance.

My wife and I both obtained matching 20-year policies via policy genius. Simply enter your information and you’ll receive real quotes from vetted life insurance companies within minutes. If you have debt and dependents, buying life insurance is one of the most responsible things you can do.

Subscribe to Financial Samurai

Pick up a copy of the USA Today national bestseller, Millionaire Milestones: Easily Reach Seven Figures. I’ve combined over 30 years of financial experience to help you accumulate more wealth than 94% of people and get out of your shell faster. As you can tell from my posts, the government loves millionaires by giving them massive health care subsidies.

Listen and subscribe to the Financial Samurai Podcast apple or Spotify. I interview experts in their fields and discuss some of the most interesting topics on this site. Thank you for sharing, rating and commenting.

To accelerate your journey to financial freedom, join over 60,000 others and subscribe Free Financial Samurai Newsletter. You can also have my posts sent to your email inbox as soon as they are published Register here.

Founded in 2009, Financial Samurai is one of the largest independent personal finance websites. All content is written based on first-hand experience and expertise.

are only shipped!")