When it comes to decision When to get Social Security Benefitsthe questions most people ask themselves are:

Would it be better to get social security at 62 or 67?

This is one of the most important decisions you make during your retirement year. It may affect your monthly income for the rest of your life, especially considering the increase in life expectancy and the increase in cost of living.

This article will help you evaluate Pros and Cons Compared to the full retirement age that waited until the age of 67, claiming social security at the age of 62. We will also look at personal and financial factors that may influence your decision.

What you need to know about Social Security Retirement Age

Social Security Benefits Allow you to start claiming pensions as early as 62 years old, but your benefits amount will be Permanent reduction If you submitted before you Full retirement age (FRA) – For most people today, this is 67. Conversely, if you postpone your FRA until 70, your earnings will grow.

Here is a quick summary:

- 62 – The earliest age, the highest 30% reduction in permanent benefits.

- 67 – Full retirement age (FRA), you will receive 100% of the main insurance amount.

- 70 – Latest Social Security Age; After FRA, annual delayed earnings increased by 8%.

- For personalized estimation, use SSA Social Security Retirement Estimator.

Receive social security at the age of 62

✅Request the Advantage of 62

- Early income

Starting at 62, you can earn early income. If you need funds due to retirement, work loss, health problems, or other personal circumstances, financial relief can be provided at the age of 62. - More checks received

Claim of 62 instead of 67 means receiving 60 monthly checks More than five years. Even if each check is small, the cumulative gains may be balanced – especially if you are not living in the mid-70s. - More time to enjoy retirement

Not everyone can live long enough to see what is called “labour age”, the age of larger checks you receive in FRA or after will catch up with the smaller checks you receive from 62 years old. Early gains may mean years of more active during retirement.

❌The disadvantages of asking for 62

- Permanently reduce welfare

Claim 62 can reduce your gains by up to 30%. For example, if your FRA benefit is $2,000, or 67 years old, you may only be able to charge about $1,400 per month from about $1,400 starting at 62. The $600 difference will continue. - Reduce income test if still working

If you plan to work while requesting before FRA, Social Security has a Income Test. In 2025, the limit is approximately $22,320; every $2 above that limit will reduce your earnings by $1. Check SSA’s Detailed information about the income test calculator. - Smaller spouse and survivor benefits

Your Social Security Benefits will also affect your spouse or survivor. Claiming that early reductions spouse and survivor benefits – so if you have a lower spouse or someone who depends on your income, this is a big weight factor.

Receive social security at the age of 67

✅Request the Advantage of 67

- Monthly earnings

Claiming your FRA (now 67, who will now be close to retirement) means you get the full benefit, which is 100% of your income in your working career. - Lifetime benefits if you live longer

People living in the mid-80s or above may get more money by waiting. Let’s look at a quick example:

| Age claim | Monthly earnings | Total number of receipts before age 85 |

| 62 | $1,400 | $386,400 |

| 67 | $2,000 | $432,000 |

By the age of 85, waiting for a claim at 67 could give you a net price of nearly $46,000.

- Spouse and Survivor Welfare

By delaying, you also increase the amount of benefits your surviving spouse will receive after you die – which is especially important if they rely on your interests as part of their income.

❌The disadvantages of waiting 67

- Revenue delay

If you need income to pay for the early 60s, then delays may require savings, 401(k), or other investments. This may put you in the face of market volatility and tax impacts. - Uncertain health or life expectancy

If you have health problems or family history means shorter life span, delays may mean less total. - Lack of early retirement opportunities

If you want to enjoy a travel or a new retirement experience early (though physically capable), you may receive a 62% more income than you get a monthly income of 67 years old.

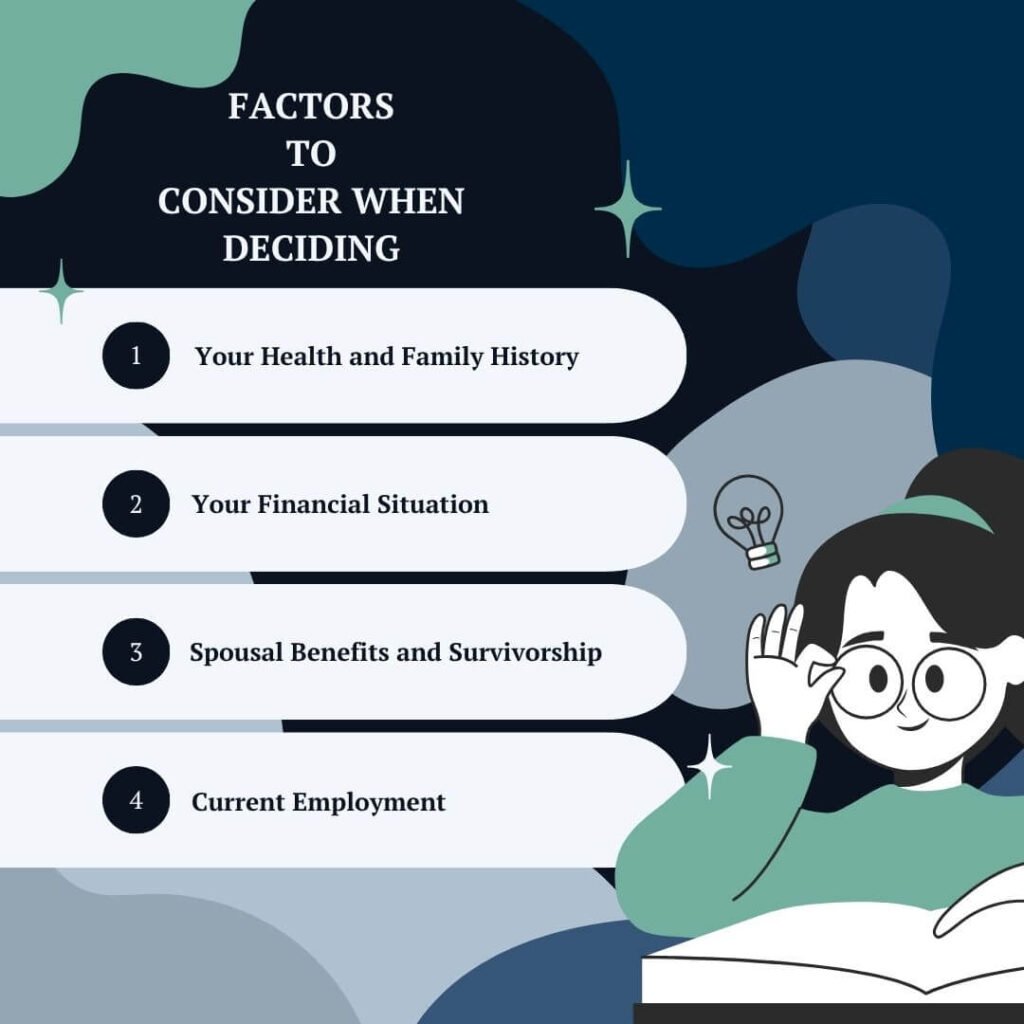

Factors to consider when deciding

1. Your health and family history

If you have good reason to believe that you will live in the mid-80s or above, then waiting may make sense. On the other hand, asking a 62-year-old may help you maximize the total dollar you receive if you face health challenges.

2. Your financial situation

Do you need income to live in? If so, claim early on that you can help. But if you have savings and other sources of income (pension, investment), then waiting can improve your Social Security benefits – providing a larger, inflation-adjusted source of income for later retirement.

3. Spousal welfare and survival

If you are a high-income spouse, delaying to FRA or 70 can increase the benefits of the surviving spouse.

4. Current employment

If you are still working and earning a lot of income before, early claims can lower your interests due to income testing. Wait until the FRA eliminates this problem.

Analysis and analysis

The key part of the decision is to calculate yours Balance point – If you wait, the age of total revenue will be greater than the age you previously claimed to have received.

Assume this is a simplified example:

- Benefits of 62 years old: $1,400/month

- Benefits of 67: $2,000 per month

In five years between 62 and 67, you will get $84,000 ($1,400 x 60 months).

To make up the $84,000 difference, a monthly check of $600 ($2,000-$1,400) you need 140 months or about 11.7 years.

This means you are about 78.7 years old.

If you live at 79 years old, wait for the reward. If not, claiming that earlier may result in more total dollars.

Inflation and Coke impact

The benefits of social security are Inflation adjustment By annual Cost of Living Adjustment (COLA). Waiting for social security benefits means getting a larger base amount each year to grow coke, which can be a huge relationship with age and expenses.

Real world situation

Program 1: Health issues

Mary, 61, has been suffering from health fears recently and did not expect to be over 75 years old. At 62, she was able to provide her with the most income and give her the most money in a shorter expected lifespan.

Plan 2: A strong family history of life span

Mark is also 61 years old, from a long-term family – most of his relatives lived into the 90s. Waiting 67 or even 70 times may bring greater benefits, which will be well supported in his later years.

There is no suitable answer. The decision to accept social security at 62 or 67 is highly personal. It depends on you Health, financial needs, life expectancy, marital status and retirement goals.

If you are unsure which avenue to choose, talk to a trusted financial advisor or explore tools like SSA Retirement age chart and other online calculators. They will help you model different options and choose the one that suits you.

Remember – this is a permanent choice. Take some time, do research, and make sure you feel comfortable before you claim it. Retirement is one of the most meaningful chapters of your life – you should prepare yourself for your utmost safety and enjoyment. It is important to plan carefully so that whatever path you choose can match your goals for a safe and fulfilling retirement.

You can also read:

*The 15 best hobbies are the elderly at home to keep them busy and happy

*The best 10 pieces of dress code idea: What to wear for retirement parties?

*The idea of best retirement party decoration makes it memorable

Source link