Thanks to everyone who responded to the recent book giveaway. Your words of encouragement and kindness are inspiring. These responses gave me a lot of topics to focus on in 2025. Congratulations to the winners.

Also, a few weeks ago I asked you to help me reach 1,000 subscribers on YouTube. The response was incredible and pushed me over the top that day! Thanks. I’ve passed 1,200 and I’m looking forward to the next milestone.

Every January for over 20 years, I analyze my portfolio and make adjustments when necessary.

Why January?

December was too busy for me. January is the calm after the holiday storm, and many of us use this time to rethink our finances.

DIY investors should consider rebalancing their portfolios annually, but no more frequently than once a year.

A lower frequency is fine. However, rebalancing should be systematic and independent of emotional triggers such as market fluctuations or personal events.

Your rebalance date can be every 18 or 24 months. Choose your rebalancing frequency, set reminders, and do it methodically. Every twelve months is a good rule of thumb, but it doesn’t have to be around the New Year.

An annual portfolio review is more than just rebalancing. My portfolio is not where I want it to be yet. Therefore, I use an annual rebalancing process to simplify.

I streamlined by:

- Reduce fund redundancy and overlap and integrate into core portfolios.

- Sell individual stocks that no longer meet my investment objectives and move funds into core index holdings.

multiple accounts

a frequently asked question If you have multiple accounts and brokers, portfolio rebalancing will determine your current asset allocation.

One way to solve this problem is to rebalance each account individually. This method is cumbersome when some accounts are much smaller than others. I prefer to rebalance by considering all my assets together.

But you can’t rebalance to a target asset allocation without knowing your current asset allocation.

Downsizing to fewer accounts and holdings can make the rebalancing process easier.

Between Ms. RBD and myself, we have:

- Two taxable accounts

- Two traditional IRAs

- Two Roth IRAs

- Two accounts sponsored by previous employers

- A SEP IRA

We have some room here to merge accounts and will do so in due course.

To make things more manageable, I only invest in one fund (total market fund) in the smaller account and then use the larger account to adjust to reach our target asset allocation.

I use a few different tools to get a comprehensive view of all our holdings and use this data to adjust our portfolio.

Find your current asset allocation

The first step in rebalancing is determining your current asset allocation.

If all your money is in one place, this can be an easy task. Some agents are very good at this. But it’s more challenging if your funds are in multiple accounts with multiple account providers.

For example, I’ve spoken with people who had part of their retirement savings in an IRA and a financial advisor, but another part was self-managed through an employer-sponsored account or a personal investment account.

I have six accounts with Fidelity and it works amazingly bad job Provides me with portfolio insights across multiple accounts. It becomes even more difficult if your account is not covered by a prime broker.

For years I’ve turned to tools to solve this problem. DIY planning tools like Boldin and ProjectionLab don’t yet offer this functionality, so we had to look for other tools.

The three tools I use are the focus of a companion video I created for this article. Please check it out on YouTube or below.

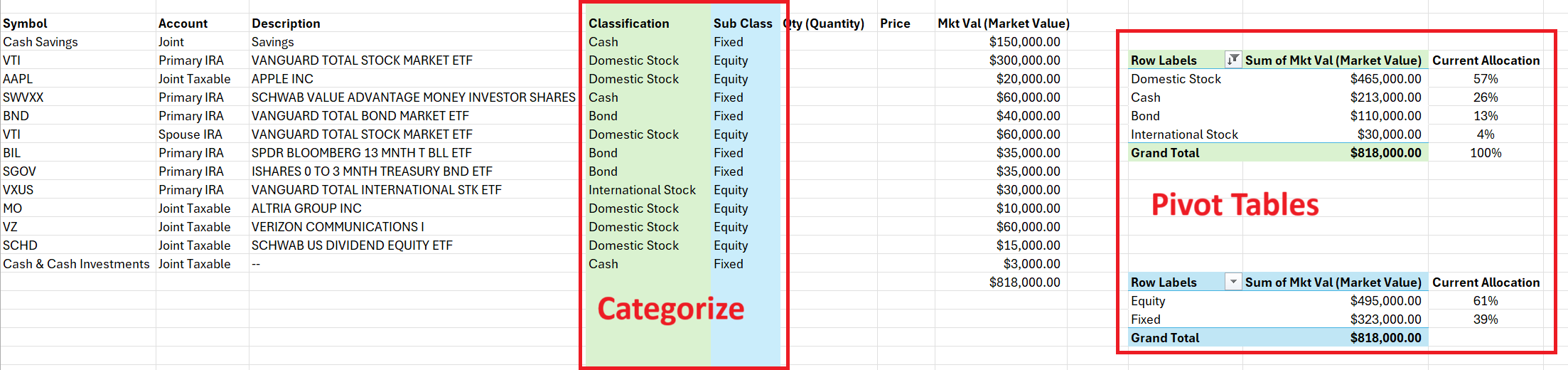

spreadsheet

I use the spreadsheet method to build charts on my portfolio page, but I’m slow to update it regularly because making charts like this is a pretty painstaking process:

The process requires (see video):

- Download spreadsheet files from holdings view across multiple brokerage accounts

- Combine all holdings and market capitalization into one table

- Insert columns and categorize each holding (manually)

- Then, use the pivot table to calculate the current allocation percentage.

Spreadsheets are free, customizable, and familiar to most people, so they are a suitable choice. But the more complex your financial situation, the more manual this process becomes.

I more frequently choose tools to help analyze my finances because they are more efficient than most spreadsheets I can build.

Morningstar Investors (Paid) is a new tool I’m trying and loving so far. It does an excellent job of integrating data and providing portfolio insights.

Empower (Free, but with a caveat) Does a great job of aggregating account profiles, as well as other analytical features.

Morningstar Investors

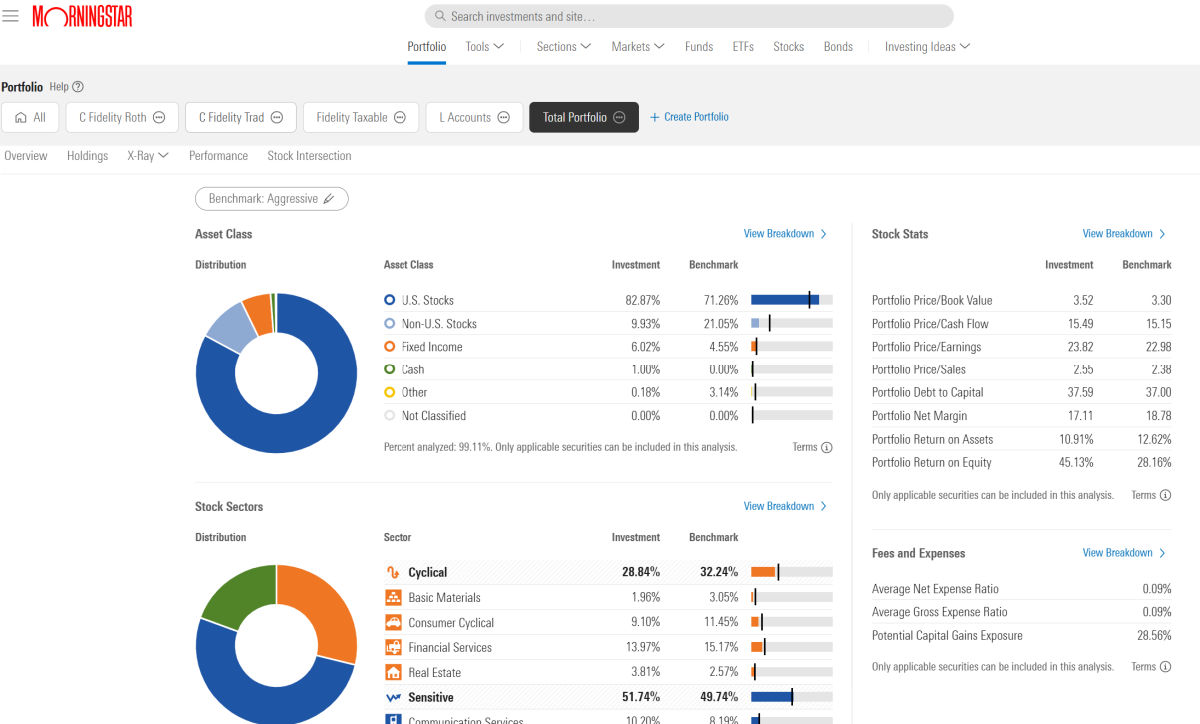

Morningstar Investor is the flagship portfolio tracked on the Morningstar website. Known for its fund ratings and retirement insights, Morningstar imports your portfolio data from multiple sources (via third-party connections) and provides comprehensive analysis.

For example, I have linked six of my Fidelity accounts, my wife’s two accounts, and my M1 Finance account. I then merged them all into one portfolio view (demonstrated in the video).

It automatically categorizes each fund and ETF and provides your current asset allocation. It can also look at every mutual fund or ETF you own and pull out individual stock insights, then show you the overlap between your holdings.

It also provides benchmark portfolios for comparison. I prefer a more personalized target asset allocation:

- 75% US stocks

- 15% international stocks

- 10% bonds

The tool quickly told me that my portfolio was overweight U.S. stocks and underweight international stocks and bonds.

Now, I can adjust my retirement accounts.

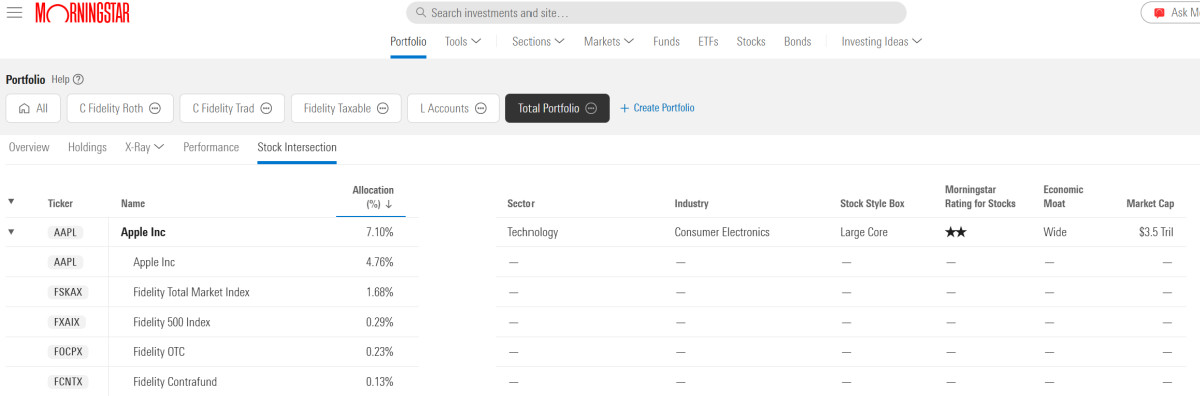

As a reward, stock crossing This tool shows which funds hold stocks and how many shares they hold, based on the amount of money you invest in the funds.

For example, I own Apple stock and several funds that hold Apple stock. This tool shows me my total exposure to all of my Apple holdings.

This is the first tool I’ve seen that does the following:

Subscribers can click on any individual holding to find fund and stock reports, proprietary ratings, charts and key statistics.

New users can get 14 day free trial. After that, the price is $199 for the first year.

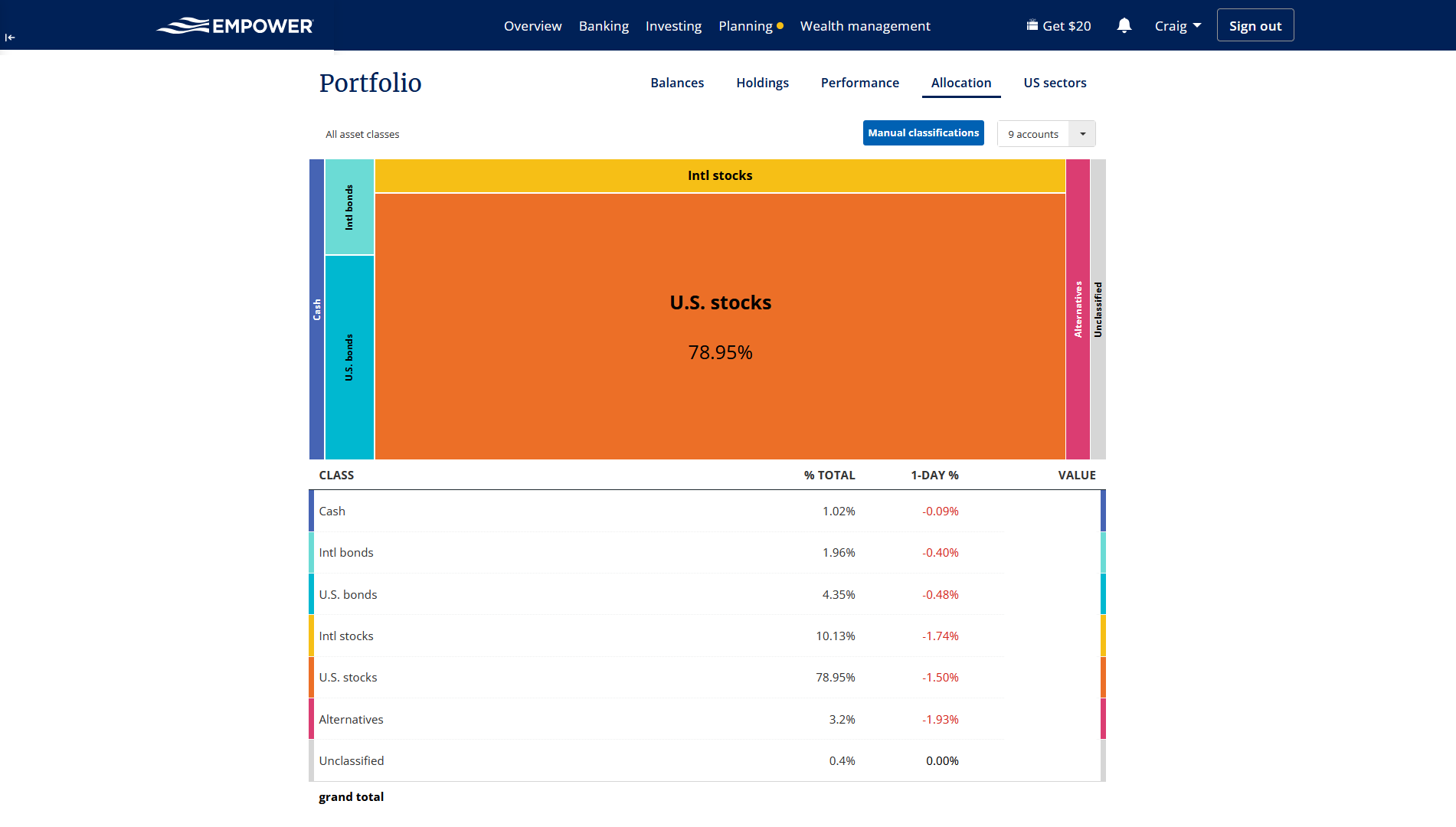

Empower

Empower is a free tool that I’ve been using for about 10 years. Formerly known as Personal Capital, Empower is a portfolio aggregator and net worth tracker that analyzes all your financial accounts into visuals.

The tool also automatically categorizes your investments, but it doesn’t give you the granularity that Morningstar does within funds (it doesn’t have stock crossing equal).

This is the view I demonstrate in the video:

Empower is a little more difficult to categorize investments, but users can modify the categories to their liking and select which accounts to include in the view.

Empower is a little more difficult to categorize investments, but users can modify the categories to their liking and select which accounts to include in the view.

In this case, I can see where my portfolio is not aligned with my goals and I can adjust my holdings.

Empower is free to use. It supports third-party data connections so you can bring in all your accounts for comprehensive analysis. Connectivity has improved recently.

It also has a nice retirement calculator, similar to Boldin or ProjectionLab, but more customizable or powerful.

The main drawback of Empower is that it is a lead generation tool for the company, which provides wealth management services.

Therefore, if you register and link your accounts, you may be contacted by a wealth advisor. Saying “no” is fine, but some people see it as an intrusion. Most people agree with this trade-off because it’s a powerful free tool.

Determine your target asset allocation

Your ideal target asset allocation is the percentage of your portfolio’s assets invested in stocks, bonds, and cash.

We can determine our asset allocation using a simple rule of thumb (which I call “minus your age”) that takes into account age and risk tolerance.

To find your ideal asset allocation, subtract your age Comes from one of the following numbers related to your risk tolerance:

- Conservative – 120

- Medium – 130

- Aggression – 140

The result is the amount allocated to the stock. The balance is then invested in bonds or other fixed assets.

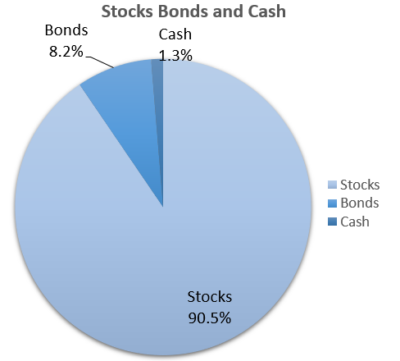

For example, I have a high risk tolerance and I’m 49 years old.

=140 - 49 = 91

So, my target is about 91% stocks and 9% bonds. See above.

Rebalance your target allocation

Once you determine your current asset allocation and goals, calculate the difference between the two. Then, go into your brokerage account and make adjustments.

In the video example, I use the following example, broken down to include U.S. stocks, international stocks, bonds, and cash:

After calculating the difference, the final step is to go into your brokerage account and:

- $56,000 Domestic Stock Fund Sold

- Sell/transfer $49,400 cash held in money market account

- Buy $53,600 worth of bond funds

- Purchased $52,800 in international stocks

As I point out several times in the film, this isn’t necessarily an exact exercise. The market fluctuates every day. But you want to get closer to your target asset allocation once a year to maintain your retirement plan.

Why do we need to rebalance?

Craig Stephens

Craig is a former IT professional who gave up a 19-year career to become a full-time financial writer. He has been a DIY investor since 1995 and founded Retire Before Dad in 2013 as a creative outlet to share his portfolio. Craig studied finance at Michigan State University and lives in northern Virginia with his wife and three children. Read more.

Favorite tools and investment services (sponsored):

Bolding — Spreadsheets are not enough. Build financial confidence. (review)

Morningstar Investors — Trust Fund and ETF Research + Portfolio Tracking. 7-day free trial.

Determine dividends — Free download to research dividend stocks (review):

Fund rises — Simple real estate and venture capital investments from just $10. (review)